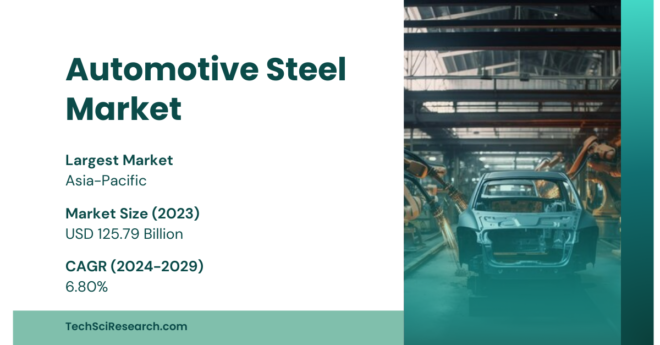

The global automotive steel market has demonstrated remarkable growth, with its market size reaching USD 125.79 billion in 2023. Forecasts indicate continued expansion to USD 186.47 billion by 2029, driven by a compound annual growth rate (CAGR) of 6.80%.

The rising demand for lightweight, high-strength materials, advancements in steel production technologies, and the growing emphasis on sustainability are pivotal in shaping this market. This report delves into the factors influencing this growth, emerging trends, and the challenges faced by industry stakeholders.

Automotive Steel Market Overview

The Role of Steel in Automotive Manufacturing

Steel has long been a cornerstone of the automotive industry, renowned for its versatility, strength, and cost-effectiveness. With increasing consumer and regulatory focus on fuel efficiency, safety, and environmental sustainability, the industry is transitioning toward advanced high-strength steels (AHSS) and ultra-high-strength steels. These materials enable manufacturers to reduce vehicle weight while maintaining structural integrity and enhancing crash performance.

Key Automotive Steel Market Drivers

- Lightweight and High-Strength Steel

Automakers are prioritizing the use of advanced materials to meet evolving performance and regulatory requirements. Lightweight, high-strength steels are essential in designing vehicles that balance fuel efficiency, safety, and durability. This trend is especially pronounced in electric and hybrid vehicles, where weight reduction directly impacts battery range and efficiency.

Browse over XX market data Figures spread through XX Pages and an in-depth TOC on the ” Global Automotive Steel Market” @ https://www.techsciresearch.com/report/automotive-steel-market/19211.html

- Sustainability and Environmental Concerns

Sustainability is reshaping the automotive steel market. Steel’s recyclability and advancements in eco-friendly production methods have strengthened its position as a preferred material. Electric arc furnace (EAF) technology, which relies on recycled scrap steel, has gained prominence due to its lower carbon emissions compared to traditional methods.

- Growing Automotive Production

The global automotive industry’s expansion, particularly in emerging economies, fuels demand for steel. Asia-Pacific’s robust vehicle manufacturing sector, led by China, India, Japan, and South Korea, continues to drive market growth. The rise of electric vehicles (EVs) further underscores the need for innovative steel solutions.

Challenges in the Automotive Steel Market

Volatility in Steel Prices

Fluctuations in raw material costs and disruptions in supply chains create uncertainty for manufacturers. These price dynamics pose significant challenges in maintaining profitability and managing operational costs.

Competition from Alternative Materials

Materials such as aluminum and composites are gaining traction due to their lightweight properties. As automakers explore these alternatives, steel producers must innovate to retain market relevance.

Stringent Environmental Regulations

Compliance with increasingly strict emissions and environmental standards requires continuous innovation in production processes and materials. Steel manufacturers must align with automakers’ sustainability goals to remain competitive.

Automotive Steel Market Segmentation

By Process

Basic Oxygen Furnace (BOF)

The BOF process is a traditional steel production method involving the conversion of molten iron into steel using oxygen. It is well-suited for large-scale production and is widely used for structural components, body panels, and chassis.

Electric Arc Furnace (EAF)

The EAF process primarily utilizes recycled scrap steel, offering greater flexibility in producing high-quality materials. Its environmental benefits, including reduced carbon emissions, make it ideal for advanced high-strength steel (AHSS) and specialized applications.

By Product

-

Low-Strength Steel: Used in less critical automotive applications.

-

Conventional High-Strength Steel (HSS): Balances strength and ductility for structural applications.

-

Advanced High-Strength Steel (AHSS): Combines superior strength and reduced weight, critical for fuel-efficient vehicles.

-

Others: Includes ultra-high-strength steel and alloyed materials.

By Vehicle Type

-

Passenger Cars: Dominant segment due to high production volumes and diverse applications of steel.

-

Commercial Vehicles: Growing adoption of AHSS for durability and load-bearing capabilities.

By Region

Asia-Pacific: A Growth Hub

Asia-Pacific leads the global automotive steel market, driven by:

-

Strong vehicle production in China, India, Japan, and South Korea.

-

Rising adoption of EVs, necessitating lightweight materials.

-

Expanding infrastructure and a growing middle class, particularly in China and India.

North America and Europe

North America and Europe remain key markets due to advanced automotive manufacturing capabilities, stringent regulations, and a focus on sustainability. Steel producers in these regions emphasize innovation to meet high-performance standards.

Other Regions

Emerging markets in Latin America, the Middle East, and Africa offer growth opportunities, supported by increasing vehicle production and infrastructure development.

Technological Advancements in Steel Production

Ultra-High-Strength Steels

Recent advancements in ultra-high-strength steels allow manufacturers to produce lighter vehicles without compromising safety. These materials play a vital role in meeting modern automotive demands.

Innovations in Manufacturing Techniques

Improved manufacturing processes, such as hot stamping and advanced rolling methods, enable precise material properties tailored to automotive needs. These innovations enhance cost efficiency and performance.

Collaboration with Automakers

Steel manufacturers are increasingly collaborating with automakers to develop customized solutions that address specific vehicle requirements, from crash performance to energy efficiency.

Emerging Trends in Automotive Steel Market

- Focus on Electric Vehicles (EVs)

The EV revolution is transforming the automotive steel market. High-strength, lightweight steels are crucial for optimizing battery performance and meeting safety standards in EVs.

- Sustainability Initiatives

Environmental concerns are driving efforts to minimize the carbon footprint of steel production. Companies are investing in greener technologies and emphasizing the recyclability of steel.

Regional Developments

Asia-Pacific’s Dominance

The Asia-Pacific region’s leadership in vehicle production and innovation underscores its critical role in the automotive steel market. Notably, China’s investment in EV infrastructure and India’s policy reforms support sustained growth.

Strategic Partnerships

In February 2024, Kobe Steel and China Baowu Steel Group explored a joint venture to strengthen their position in the EV segment. Such collaborations highlight the strategic moves by key players to capitalize on market opportunities.

Download Free Sample Report @ https://www.techsciresearch.com/sample-report.aspx?cid=19211

Customers can also request 10% free customization on this report.

Major Players in the Global Automotive Steel Market

Key Companies

-

ArcelorMittal SA: A leader in advanced steel solutions.

-

China Steel Corporation: Prominent in Asia’s growing automotive sector.

-

JFE Steel Corporation: Innovating in AHSS and lightweight materials.

-

NIPPON STEEL CORPORATION: Known for its focus on sustainability and high-performance steels.

-

Nucor Corporation: A pioneer in EAF-based steel production.

-

Tata Steel Limited: A major player in emerging markets.

-

United States Steel Corporation: Strong presence in North America.

-

Grow Ever Steel (India) Private Limited: Expanding its footprint in India.

-

Hyundai Steel Co., Ltd.: Leader in advanced steel for automotive applications.

-

Steel Dynamics, Inc.: Focused on innovative and sustainable steel solutions.

Future Outlook

Market Projections

The global automotive steel market is poised for sustained growth, driven by technological advancements, regional developments, and the transition toward greener vehicles. By 2029, the market is expected to reach USD 186.47 billion, reflecting its critical role in the automotive industry.

Strategic Recommendations

-

Innovation: Steel manufacturers must continue investing in research and development to create materials that meet evolving automotive needs.

-

Sustainability: Emphasizing eco-friendly production processes and recycling will enhance competitiveness.

-

Partnerships: Collaboration with automakers is essential for developing tailored solutions and maintaining market relevance.

Conclusion

The automotive steel market is at a transformative juncture, driven by the demand for innovative materials and the push toward sustainability.

As automakers embrace electric and hybrid vehicles, steel producers have an opportunity to redefine their role in the industry. By focusing on advanced high-strength steels, sustainable production methods, and strategic collaborations, the industry can navigate challenges and capitalize on emerging trends.

The future of automotive steel lies in its ability to adapt, innovate, and contribute to the next generation of vehicles.

You may also read:

Used Bikes Market Insights: USD 44.61 Billion with Projected 7.57% CAGR Growth

Vehicle Tracking System Market Forecast: USD 25.35 Billion (CAGR: 7.28%)

Automotive LED Lighting Market In-depth Analysis: Size, Growth, & Forecast for 2029 (CAGR: 5.80%)